News from Los Azules are getting better and better - now we have a new PA with increased NPV of this project from just under 500 million to 2.8 billion us dollars! Two out of five planned drills will be on the site shortly and deposit will grow even more in its size.

Now we can realise why TNR Gold was so determined in its legal fight for the back-in right into this deposit. At stake now is up to 15% of the project (12.5% technically, but with high grade core on the former TNR Gold - Xstrata land) with value of 420 million dollars, according to this latest estimations from Minera Andes. There is a legal risk in every lawsuit and our position is that the court should always decide about the property ownership between TNR Gold and Minera Andes, but for the junior with market cap just over 20 million CAD it could be a very important development - the higher the value of the prise the higher the chances of out-of-the-court settlement. We will be really surprised if Rob McEwen will drag this project along into the court battle - which date is set for the June 2011 - increasing its value further with announced drilling program.

George Macintosh Q.C. is leading TNR Gold litigation team. His personal engagement and new twist in litigation strategy, "that "production of a feasibility study, whether produced within 36 months or some other time, was a condition solely for the benefit of Solitario (TNR Gold sub - S.), and as such, could be waived" - provides nessesary support that TNR Gold legal claims to the part of 2.8 billion NPV story of Los Azules should be taken seriously.

To view a copy of George Macintosh’s biography please click here.

The recent professional award shows that TNR Gold shareholders are in the right company to defend thier property rights in this legal case, which some people are already calling "MAI's bullying tactics are on trial here. It is truly a 'David and Goliath' case." We will address you to the Statement of Defence by TNR Gold and Los Azules propery maps on the links below to make you own conclusions, as always.

"TNR Gold Corp.'s litigation in the Supreme Court of British Columbia related to the Los Azules project in Argentina, involving TNR, Minera Andes Inc., MIM Argentina Exploraciones S.A. (Xstrata) and related entities, has been joined for hearing and scheduled for a new trial date of June 20 to July 15, 2011. The trial will be held in Vancouver."

"It is important to remember, that now, according to this NR, all litigation around Los Azules between TNR Gold, Minera Andes and Xstrata is joined in one trial and TNR Gold will seek, according to the Statement of Defence above, not only rectification of the option agreement to reflect its true intentions - without 36 months condition, but that "production of a feasibility study, whether produced within 36 months or some other time, was a condition solely for the benefit of Solitario (TNR Gold sub - S.), and as such, could be waived".

Also at stake is Escorpio IV property:

"We did not understand why Minera Andes did not accepted the back in right by TNR Gold and lost opportunity to consolidate the project and secure a very important Escorpio IV property, where according to Minera Andes mining plan part of mining facilities supposed to be located, but Rob McEwen must has his own strategy. With this kind of presentation it will be not cheap any more to settle out of the court, but it is always better then drag such a project in litigation for years to come."

Now we can realise why TNR Gold was so determined in its legal fight for the back-in right into this deposit. At stake now is up to 15% of the project (12.5% technically, but with high grade core on the former TNR Gold - Xstrata land) with value of 420 million dollars, according to this latest estimations from Minera Andes. There is a legal risk in every lawsuit and our position is that the court should always decide about the property ownership between TNR Gold and Minera Andes, but for the junior with market cap just over 20 million CAD it could be a very important development - the higher the value of the prise the higher the chances of out-of-the-court settlement. We will be really surprised if Rob McEwen will drag this project along into the court battle - which date is set for the June 2011 - increasing its value further with announced drilling program.

George Macintosh Q.C. is leading TNR Gold litigation team. His personal engagement and new twist in litigation strategy, "that "production of a feasibility study, whether produced within 36 months or some other time, was a condition solely for the benefit of Solitario (TNR Gold sub - S.), and as such, could be waived" - provides nessesary support that TNR Gold legal claims to the part of 2.8 billion NPV story of Los Azules should be taken seriously.

30 NOVEMBER 2010

BEST LAWYERS NAMES GEORGE MACINTOSH AS ONE OF THE 2011 LAWYERS OF THE YEAR

Best Lawyers, the oldest peer-review publication in the legal profession, has named George Macintosh, Q.C. as the “Vancouver Best Lawyers Bet-the-Company Litigator of the Year” for 2011.

“The lawyers being honoured as “Lawyers of the Year” have received particularly high ratings in our surveys by earning a high level of respect among their peers for their abilities, professionalism, and integrity” states Best Lawyers.

The recent professional award shows that TNR Gold shareholders are in the right company to defend thier property rights in this legal case, which some people are already calling "MAI's bullying tactics are on trial here. It is truly a 'David and Goliath' case." We will address you to the Statement of Defence by TNR Gold and Los Azules propery maps on the links below to make you own conclusions, as always.

"TNR Gold Corp.'s litigation in the Supreme Court of British Columbia related to the Los Azules project in Argentina, involving TNR, Minera Andes Inc., MIM Argentina Exploraciones S.A. (Xstrata) and related entities, has been joined for hearing and scheduled for a new trial date of June 20 to July 15, 2011. The trial will be held in Vancouver."

"It is important to remember, that now, according to this NR, all litigation around Los Azules between TNR Gold, Minera Andes and Xstrata is joined in one trial and TNR Gold will seek, according to the Statement of Defence above, not only rectification of the option agreement to reflect its true intentions - without 36 months condition, but that "production of a feasibility study, whether produced within 36 months or some other time, was a condition solely for the benefit of Solitario (TNR Gold sub - S.), and as such, could be waived".

Also at stake is Escorpio IV property:

"We did not understand why Minera Andes did not accepted the back in right by TNR Gold and lost opportunity to consolidate the project and secure a very important Escorpio IV property, where according to Minera Andes mining plan part of mining facilities supposed to be located, but Rob McEwen must has his own strategy. With this kind of presentation it will be not cheap any more to settle out of the court, but it is always better then drag such a project in litigation for years to come."

"Los Azules emerges in this light as a very important Copper deposit with a lot of upside in its valuation among the leaders in this particular quality, relatively high CAPEX requirements, but in the solid middle or to the higher band in a lot of different investment metrics compare to the other juniors in the analysis provided by CIBC."

It is very important that, according to CIBC report page 42, legal claims of TNR Gold are communicated properly within the industry now. Junior can fully rely on its litigation strategy, court decision or potential out-of-the-court settlement, should Minera Andes decide to clean the house before calling the real estate agents.

We will always leave it to the lawyers and court to decide - who owns what in this case in its proper time.

Copper is going up and the deposit is growing - we guess that nobody is in a hurry here. Argentina will become more fluent in Mandarin and the value of every lb of Copper in the ground will go up - to reflect fundamental picture described in the CIBC report."

Please, do not forget, that we own stocks we are writing about and have position in these companies. We are not providing any investment advise on this blog and there is no solicitation to buy or sell any particular company here. Always consult with your qualified financial adviser before making any investment decisions.

We will always leave it to the lawyers and court to decide - who owns what in this case in its proper time.

Copper is going up and the deposit is growing - we guess that nobody is in a hurry here. Argentina will become more fluent in Mandarin and the value of every lb of Copper in the ground will go up - to reflect fundamental picture described in the CIBC report."

Please, do not forget, that we own stocks we are writing about and have position in these companies. We are not providing any investment advise on this blog and there is no solicitation to buy or sell any particular company here. Always consult with your qualified financial adviser before making any investment decisions.

MineWeb:

Minera Andes Los Azules deposit could be major copper mine - McEwen

Minera Andes CEO Rob McEwen says the company's Los Azules property lies among the world's copper giants. A preliminary assessment suggests it also may be a candidate.

Minera Andes estimates $2.8-billion (U.S.) Azules NPV

2010-12-16 16:12 ET - News Release

Mr. James Duff reports

MINERA ANDES ANNOUNCES UPDATED PRELIMINARY ASSESSMENT FOR ITS LOS AZULES COPPER DEPOSIT

Minera Andes Inc. has released the results of an updated preliminary assessment on its 100-per-cent-owned Los Azules copper project located in the San Juan province of western-central Argentina. It is based on the updated resource estimate announced in Stockwatch in June, 2010, and higher base case metal price assumptions. Amounts are in U.S. dollars unless otherwise stated.

Highlights using a copper price of $3 per pound

Base case pretax net present value is $2.8-billion, and the internal rate of return is 21.4 per cent at a discount rate of 8 per cent.

Life-of-mine cash operating costs are 96 cents per pound of copper, net of gold and silver byproduct credits.

Initial capital is $2.9-billion.

Capital payback is in three years.

Mine life is 25 years.

Rob McEwen, chairman and chief executive officer of Minera Andes, said: "We are advancing the engineering studies on Los Azules to systematically derisk the project. The field season is just getting under way, and we are currently mobilizing the first two of five drill rigs to the project. In addition to continuing the infill and step-out drilling, we will start to test some of the newly identified deeper geophysical targets this season."

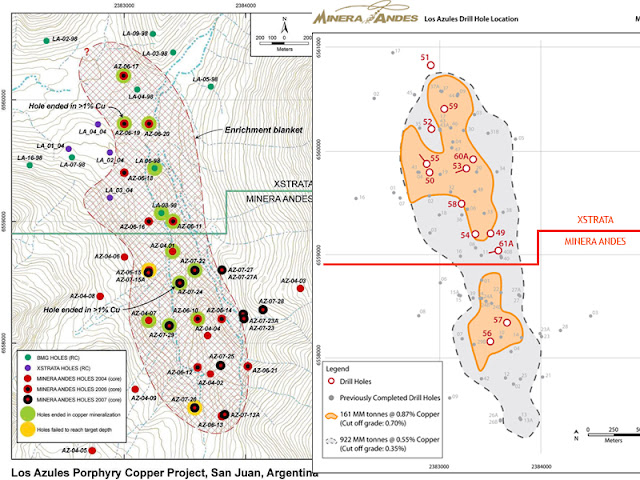

Los Azules copper project is an advanced-stage porphyry copper exploration project located in the cordilleran region of San Juan province, Argentina, near the border with Chile. The deposit is a typical porphyry copper system in that the upper part of the system consists of a barren leached cap, which is underlain by a high-grade secondary enrichment blanket, and the primary mineralization below the secondary enrichment zone extends to at least 650 metres, which are the depth of the deepest holes drilled to date. The deposit is approximately one kilometre wide by four kilometres long, and it is open in several directions.

Highlights of the updated preliminary assessment are shown in the attached table. Details may be found in an updated technical report which will be posted on SEDAR following the issuance of this news release.

PRELIMINARY ASSESSMENT HIGHLIGHTS

NPV ($3/lb Cu, 8-per-cent discount rate) $2,826-million

IRR 21.4%

Initial capital expenditure $2,851-million

LOM average operating costs $7.82/t ore

LOM C-1 cash costs (net byproduct credits) $0.96/lb Cu mined

Nominal mill capacity 100,000 tpd

Annual throughput 36 million tonnes

Mine life 25.4 years

Life-of-mine strip ratio 1.37

LOM average annual copper-in-concentrate production 169,100 tonnes

First five years average annual copper-in-concentrate

production 226,500 tonnes

All monetary amounts are expressed in U.S. dollars unless otherwise stated.

The PA is preliminary in nature and includes the use of inferred resources,

which are considered too speculative geologically to have the economic

considerations applied to them that would enable them to be categorized as

mineral reserves. Thus, there is no certainty that the results of the PA

will be realized. Actual results may vary, perhaps materially. The level of

accuracy for preliminary assessment estimates is approximately plus or

minus 35 per cent.

Compared with the previous preliminary assessment released in March, 2009, the net present value discounted at 8 per cent has increased to $2.9-billion from $496-million, and the internal rate of return has increased to 21.4 per cent from 10.8 per cent. In addition, the payback of preproduction capital has decreased to 3.1 years from 6.4 years from the start of production.

The main driver of the improved project economics is that the base case copper price has been increased from $1.90 per pound to $3 per pound. Specifically the higher copper price added approximately $3.2-billion to the NPV, and the increased resources added approximately $2.1-billion.

The benefits of the higher copper price and increased resources were significantly offset by increases in the estimated operating costs ($695-million), capital costs ($100-million), and export retention taxes and royalties ($3.4-billion).

The updated preliminary assessment also incorporates updated property status and ownership information, revised locations for the project facilities, and an updated geological interpretation.

Project economics

The preliminary assessment contains a cash flow valuation model based upon the geological and engineering work completed to date and technical and cost inputs developed by Samuel Engineering Inc., Ausenco Vector and MTB Project Management Professionals Inc. The base case was developed using long-term forecast metal prices of $3 per pound for copper, $980 per ounce for gold and $15.60 per ounce for silver.

This news release has been submitted by Jim Duff, chief operating officer of the corporation. For further information, please contact Mr. Duff, or visit the company website.

Scientific and technical information

The information presented in this press release has been reviewed and approved by the qualified persons responsible for the technical report that presents the results of the updated preliminary assessment. They are: Kathleen Altman, PhD, PE, Robert Sim, PGeo, Bruce Davis, PhD, FAusIMM, Richard Jemielita, PhD, MIMMM, William Rose, PE, and Scott Elfen, PE. All are independent qualified persons as defined by National Instrument 43-101 (standards of disclosure for mineral projects). Mr. Sim, Mr. Davis and Mr. Rose are responsible for the mineral resource estimate. Mr. Davis is responsible for the quality control for the assaying of Los Azules drill core. All samples were collected in accordance with industry standards. Splits from the drill core samples were submitted to the ACME sample preparation laboratory in Mendoza, Argentina, and then transferred to ACME's laboratory in Santiago, Chile, for fire assay and ICP analysis. Accuracy of results is tested through the systematic inclusion of standards, blanks and check assays. Mr. Rose is responsible for developing the mine production schedule and participating in the resource estimate. Mr. Elfen of Ausenco Vector is responsible for information about environmental liabilities, environmental permitting and the geotechnical designs used for the study. Mr. Jemielita is responsible for information about the geological setting, deposit types, mineralization, exploration and drilling. Ms. Altman, Samuel Engineering, is the principal author of the report with specific responsibility for mineral processing and metallurgical testing, the capital and operating cost estimates, and the economic evaluation.

Mineral resources are generated using ordinary kriging with a nominal block size of 20 by 20 by 15 metres. Block grade estimates are derived from drill hole sample results and the interpretation of a geologic model, which relates to the spatial distribution of copper, gold, silver and molybdenum in the deposit. There are a total of 114 drill holes in Los Azules database with a cumulative length of 30,997 metres and a total of 15,260 samples analyzed for a suite of elements, including total copper, gold, silver and molybdenum. A total of 58 of the drill holes have some portion of the sample intervals tested for sequential copper analysis. This information contributed to the development of the mineral zone domains. The portion of the new mineral resource that has been defined as indicated is based on a drilling configuration that exhibits the degree of continuity required for higher-level mineral resources. Inferred mineral resources are limited to blocks within a maximum distance of 200 metres from a drill hole. As required by NI 43-101, the possible future economic viability of the mineral resource has been exhibited by restriction within a pit shell derived about the copper content in indicated and inferred class blocks at a copper price of $2.50 per pound, total operating costs of $5.25 per tonne and an average pit slope of 34 degrees. Mineral resources are presented at a cut-off grade of 0.35 per cent copper, which is the same base cut-off grade used in the 2008 mineral resource estimate. These are mineral resources, not mineral reserves.

For further information in respect of Los Azules project, please refer to the technical report entitled, "Canadian National Instrument 43-101 technical report, updated preliminary assessment, Los Azules project, San Juan province, Argentina," dated Dec. 1, 2010. This report will be made available on SEDAR concurrent with the filing of this news release.

We seek Safe Harbor.

No comments:

Post a Comment